This study, based on data from the ITC, examines the evolution and characteristics of Chinese antibiotic trade from 2002 to 2021. It explores the current state of global and Chinese antibiotic export trade, as well as China’s role and trends in the global antibiotic supply chain. The main findings from this research are as follows.

Trends in China’s antibiotic export trade

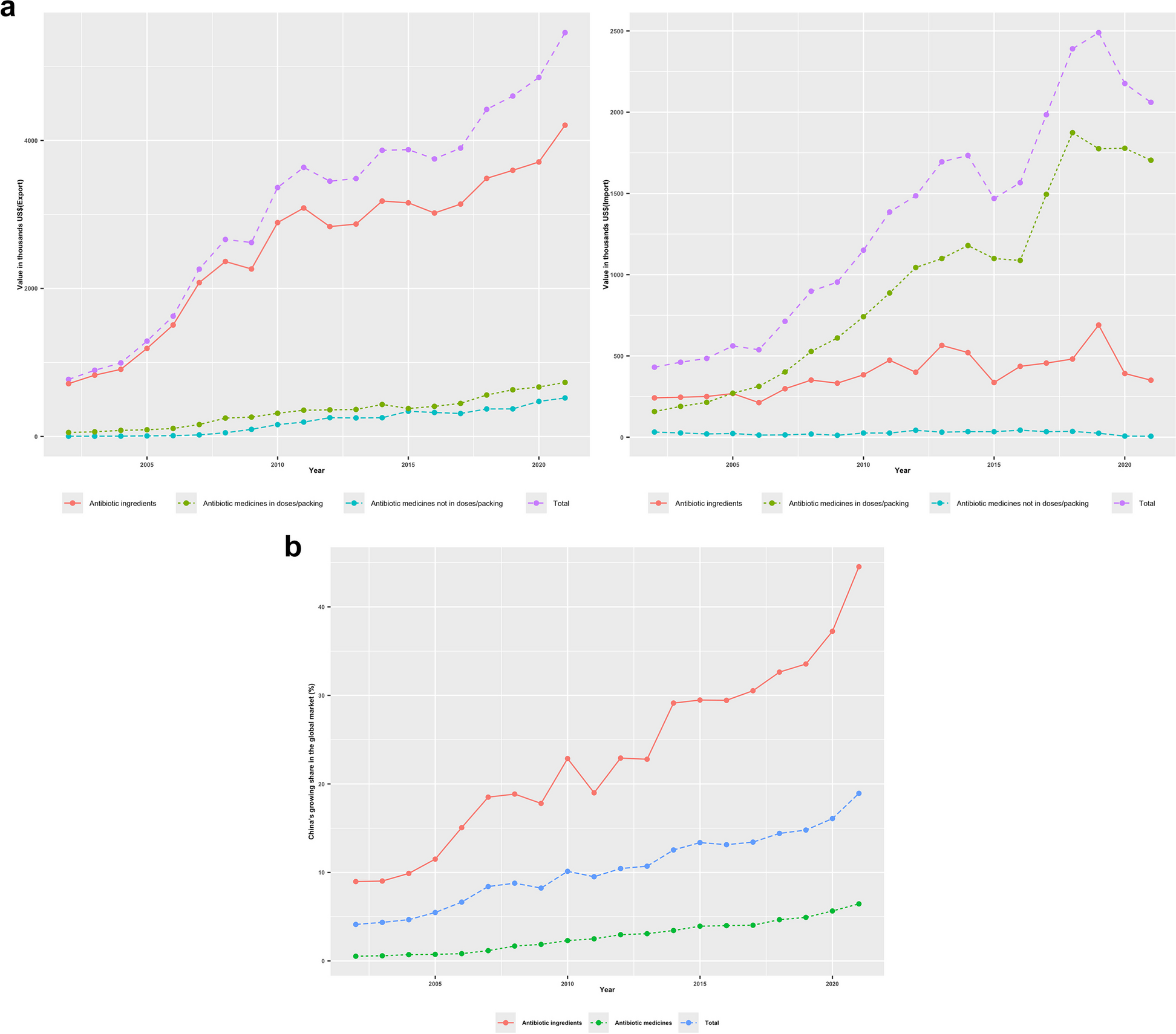

China’s export trade of antibiotics is influenced by macroeconomic policies. On the export side, the focus has primarily been on low - value ingredients [48], though the export of antibiotic medicines is expanding. The overall export value has shown an upward trend, driven largely by antibiotic ingredients. This can be attributed to a combination of factors, including market diversification, international environmental protection, demand patterns, and cost advantages [14, 49, 50]. The export of antibiotic ingredients surged after 2020, possibly due to the treatment of secondary infections and overuse during the COVID-19 pandemic [51,52,53]. The fact that, for both antibiotic medicines and antibiotic ingredients, the cumulative growth rate of the export volume is lower than that of the export value indicates a significant increase in the average unit price. This suggests ongoing industrial restructuring, with a gradual shift from lower-value to higher-value products. Additionally, the export value and proportion of antibiotic medicines vis-à-vis ingredients have been expanding since 2008. This may be linked to policies like the Medium- and Long-Term Science and Technology Development Plan (2006-2020), issued in 2006 [30], aimed at enhancing the quality of medicines. The Major Projects Plan, established in 2008, which prioritizes new drug R&D, may have also played a role [54].

On the import side, there was a significant surge in antibiotic medicines imports in 2007 and 2017, with a steady increase in antibiotic ingredient imports starting in 2016, culminating in a sharp spike in 2019. This trend can be explained by various favorable policies, including improved import regulation, reduced import barriers, initiatives to promote generic drug consistency, and supply-side structural reforms in the pharmaceutical sector [55]. Notable policy changes include the 2007 revision of the Drug Registration Regulation, the 2016 Guideline for the Consistency Evaluation of Generic Drug Quality and Efficacy, the 2017 Classification Guidance for Generic Drug Quality and Efficacy Consistency Evaluation, and the 2018 National Drug Safety 12th Five-Year Plan [56]. The implementation of drug consistency evaluations has driven demand for high-quality imported ingredients and medicines. Environmental challenges leading to shortages or price spikes for ingredients, coupled with multinational companies’ increasing procurement from overseas, have likely further spurred significant growth in imports [57]. The cumulative growth rate of imports for antibiotic ingredients and medicines is lower than that of import value, indicating an increase in average unit value. This may suggest that China's industrial structure is adjusting, with import demand remaining focused on higher-value products.

Overall, China’s antibiotic industry holds a position in the upstream-to-midstream segment of the global antibiotic supply chain [51,52,53, 58]. The worldwide supply of antibiotic ingredients is, to a substantial extent, dependent on China’s exports. China is now the world’s 7th largest exporter of antibiotic medicines and the largest exporter of antibiotic ingredients. Noticeably, India’s antibiotic ingredients are relatively dispersed [59], whereas China's antibiotic ingredient exports are relatively concentrated in a small number of markets. About 1/3 of those exports go to India, making up 82.7% of India's total imports. As a major exporter of antibiotics, India today is highly dependent on importing antibiotic ingredients from China [9]. Consequently, the antibiotic manufacturing industry in many countries relies, either directly or indirectly, on China, positioning China as a critical player in the global antibiotic supply chain. This phenomenon was illustrated in 2017, when the shutdown of a single factory in China caused a worldwide shortage of the cornerstone antibiotic piperacillin–tazobactam [20, 60].

However, this concentration of export markets heightens the reliance of Chinese exports on specific regions. If there were issues with exports to India, for example, it would be difficult to offset them through stability or counterbalancing in other export markets [50]. Presently, countries are placing more emphasis on reshoring ingredient production, which could pose challenges for China [33, 34]. Some of the most active measures are likely to come from the United States’ Biosecure Act, which will reduce US companies’ ability to do business with certain Chinese companies [61, 62]. Similarly, Indian policies to reshore API production are likely to be significant for China, given the weight of India in Chinese exports [47, 63, 64]. Equally, increasing environmental regulation of antibiotic production may also affect China [65]. It is not yet clear over what timeframe this is likely to alter the global supply structure or the potential size of the impact of measures such as these [50].

Conversely, China’s antibiotic medicine export market is not highly concentrated, with exports going to a large number of countries, indicating that it may be in a growth phase. This dispersion reduces economic risk but increases trade costs, suggesting China may lack competitive high-tech and high-value-added products [50]. Interestingly, China is also a primary export destination for other major antibiotic ingredient exporters, likely due to the domestic demand for high-quality, high-value ingredients. This points to the potential for China to optimize its product structure and focus on precision and specialization [48].

China’s antibiotic export trade network has extended to all corners of the globe, with a growing importance in developed markets like Europe and North America. The export markets for China’s antibiotic ingredients span various continents, with a strong focus on South Asia and Western Europe. The primary markets for antibiotic medicines (penicillins, streptomycins and their derivates) are developing regions such as East and West Africa, South America, and Southeast Asia. Exports to the US started to grow in 2018 and showed a sharp increase in 2020, while exports to Japan surged in 2015. As for antibiotic medicines (other antibiotics), their primary export destinations include Western Europe, North America, and South Asia. Exports to the US began to grow in 2016, showed an accelerated increase in 2018, and reached another peak in 2021. This surge might be influenced by the overuse of antibiotics during the COVID-19 pandemic [51,52,53, 58]. It also reflects the impact of consistency evaluations for generic drugs [56] and other incentive policies aimed at boosting drug R&D [30, 66,67,68], which have improved drug quality, international recognition, and competitiveness, thereby driving exports [69]. The growing importance of the European and North American markets suggests a more rational and balanced global market distribution [23, 41].

China’s competitive advantage in antibiotics

China’s competitive advantage in antibiotic ingredients is likely to remain strong, whereas antibiotic medicines remain insufficiently competitive and are expected to continue to show a comparative disadvantage in the short term. The comparative advantage of antibiotic ingredients has shown a fluctuating upward trend, primarily due to costs associated with labor and the environment [70]. The comparative advantage of antibiotic medicines has been rising since around 2007, likely due to incentives for R&D and changes in drug management policies.

From the relative index of comparative advantage, around 2006, China’s comparative advantage in antibiotics began shifting towards antibiotic medicines, but in the short term, the export advantage of antibiotic ingredients will continue to dominate. The factors behind this transition likely include technological advancements like increased labor productivity, and enhanced innovation capacity. Policy support, resource endowment, economies of scale, and ingredient costs have also played significant roles [71]. This evolution suggests that China’s antibiotic export trade structure is being optimized, transitioning towards innovation, with industrial competitiveness strengthening and moving towards the higher end of the global industrial chain [72]. From the perspective of China’s domestic industry and industrial policy, it will be important to pursue consolidation and enhanced comparative advantage, strengthen independent innovation capacity, drive technological progress, and mitigate the adverse effects of declining labor supply, rising ingredient costs, and the appreciation of the effective exchange rate [71].

A curious finding noted above is that, as well as being among the top ten exporters of antibiotic ingredients (excluding Spain and Singapore), China is also one of the main export destinations. This is a surprising finding, and possibly indicates that China is importing comparatively higher quality antibiotic ingredients from these countries, or that multinational companies in China are purchasing ingredients from outside China (Fig. 3b). More research is needed to verify this.

Global antibiotic value chains

The COVID-19 pandemic has underscored China’s centrality in the supply of many health commodities [34], reviving discussions about reshaping global production networks. Overall, from a global perspective, COVID-19 has shown the importance of diversified and resilient supply and value chains in ensuring access to key medical technologies and commodities. As discussed above, countries like the US and India have implemented a series of incentives to boost domestic production of antibiotic ingredients [33, 73]. Reshaping the supply chain may not be achieved in the short term, but in the long run, it poses challenges for Chinese policymakers and industry [34, 50]. These include strengthening independent innovation and quality certification, boosting international competitiveness, and diversifying markets and export destinations [74, 75], supported by sound policies [34].

As we highlight above, access to antibiotics is a fundamental question for global health. The lack of adequate access is assessed to cause more deaths globally than antimicrobial resistance and furthers the emergence of resistance, predominantly in LMICs [76]. Faced with this, there is a need for greater support to initiatives and coordination to improve access to the right antibiotic at the right time. This is both a consideration for global health equity and for the sustainable management of antibiotics as a global good. It is also an important consideration in the negotiation of a pandemic treaty, given the importance of antibiotics in treating secondary bacterial infections in the case of a viral pandemic as well as in the management of possible bacterial threats [2]. China’s significance in global antibiotic value chains, its huge manufacturing capability (and linked cost advantages in the supply of many health commodities), as well as its rapid scientific and technological progress, inevitably make the country an important part of arrangements that are needed to ensure equitable global access to antibiotics in the future [1].

This study also has limitations. Although volume or unit value is not found to be a relevant measure in this study, analyzing only trade value may overlook the pricing of more specific types of antibiotics in different markets and how prices may be affecting trade [36]. Additionally, the unit value of antibiotics exported from China is relatively low compared to other major antibiotic-exporting countries in Europe and America. Consequently, China’s export share of antibiotics, calculated based on export value, may be underestimated compared to calculations based on export volume.

Comments (0)